Choosing a Medigap policy can be a daunting task, especially with the myriad of options available in 2021. This comprehensive guide will help you navigate the complexities of Medigap insurance, ensuring that you make an informed decision that suits your healthcare needs and budget. In this article, we will cover everything from understanding Medigap policies, the benefits they offer, to tips on selecting the right plan for you.

Medigap, also known as Medicare Supplement Insurance, plays a crucial role in filling the gaps left by Original Medicare coverage. With various plans available, it's essential to understand the specifics of each option before making a decision. This guide aims to provide clarity on what Medigap is, how it works, and the factors to consider when choosing a policy.

As we delve into the intricacies of Medigap policies, we will provide insights into the different types of plans available, eligibility requirements, and tips for comparing costs and benefits. By the end of this article, you will be equipped with the knowledge necessary to choose the best Medigap policy for your individual needs.

Table of Contents

- What is Medigap?

- Benefits of Medigap Policies

- Types of Medigap Plans

- Eligibility Requirements for Medigap

- How to Choose a Medigap Policy

- Comparing Medigap Plans

- Cost of Medigap Insurance

- Common Medigap Misconceptions

What is Medigap?

Medigap policies are private insurance plans that help cover some of the healthcare costs that Original Medicare does not pay. This includes copayments, coinsurance, and deductibles, making them essential for many seniors seeking comprehensive health coverage. Understanding Medigap is crucial for anyone over 65 or those eligible due to disability.

Benefits of Medigap Policies

Here are some key benefits of choosing a Medigap policy:

- Reduced out-of-pocket expenses for healthcare services.

- Greater access to healthcare providers without referrals.

- Plans are standardized, making it easier to compare options.

- Guaranteed renewable coverage as long as premiums are paid.

Types of Medigap Plans

There are 10 standardized Medigap plans available in most states, labeled A through N. Each plan offers different levels of coverage, so it’s essential to understand what each one entails:

- Plan A: Basic coverage including hospital and coinsurance costs.

- Plan B: Similar to Plan A but includes coverage for the Part A deductible.

- Plan C: Comprehensive coverage including all gaps, but not available for new beneficiaries after 2020.

- Plan D: Similar to Plan C but does not cover the Part B deductible.

- Plans F and G: Offer extensive coverage options, with Plan G being the most popular among new enrollees.

- Plan K and L: Offer lower premiums but with higher out-of-pocket costs.

- Plan M and N: Provide unique coverage options with varying cost-sharing features.

Eligibility Requirements for Medigap

To qualify for a Medigap policy, you must meet the following criteria:

- Be enrolled in Original Medicare (Part A and Part B).

- Be at least 65 years old or have a qualifying disability.

- Live in the state where you are applying for Medigap coverage.

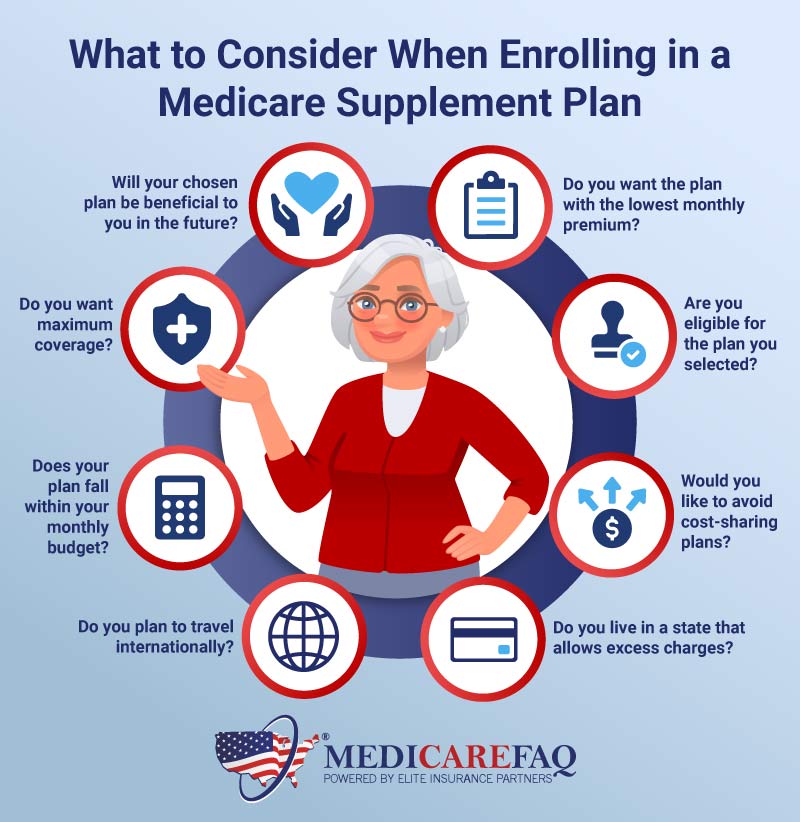

How to Choose a Medigap Policy

Selecting the right Medigap policy involves careful consideration of several factors:

- Assess your healthcare needs and expected medical expenses.

- Compare the benefits of different Medigap plans.

- Evaluate the financial stability and reputation of insurance providers.

- Consider your budget and the premiums associated with different plans.

Comparing Medigap Plans

When comparing Medigap plans, keep the following in mind:

- Look for plans that cover the services and costs you anticipate needing.

- Check the monthly premiums and any out-of-pocket expenses associated with each plan.

- Utilize online comparison tools and resources to analyze different policies.

Cost of Medigap Insurance

The cost of Medigap insurance can vary widely based on several factors:

- Your location and the insurance provider.

- Your age and health status at the time of application.

- The specific plan you choose and its coverage levels.

On average, Medigap premiums can range from $100 to $300 per month, depending on these factors.

Common Medigap Misconceptions

There are several misconceptions surrounding Medigap policies that can lead to confusion:

- Medigap is not the same as Medicaid; it is a supplement to Medicare.

- Medigap policies do not cover long-term care or vision/dental services.

- All Medigap plans are standardized, meaning the benefits will be the same regardless of the insurer.

Conclusion

Choosing a Medigap policy is an important decision that requires careful consideration of your healthcare needs and financial situation. By understanding the various options available and what each plan covers, you can make an informed choice that best fits your needs. Remember to compare different plans and providers to find the most suitable coverage.

If you have questions or would like to share your experiences with Medigap policies, please leave a comment below. Don't forget to share this article with others who may find it helpful!

Penutup

Thank you for reading our comprehensive guide to choosing a Medigap policy. We hope this information will help you navigate your healthcare insurance options with confidence. Be sure to return for more insightful articles and updates on health insurance and related topics!